Superset and the Future of Crosschain Stablecoin Liquidity and Onchain FX

Foreign exchange is already the largest financial market in the world. Average daily OTC FX turnover has reached $9.6 trillion. That market has deep liquidity, standard market conventions, and mature execution infrastructure. By comparison, onchain finance has reached a different stage of maturity. Stablecoins alone account for more than $300 billion across more than 160 chains with nonzero balances. The issue is where liquidity sits when a trade has to settle in a different asset or on a different chain.

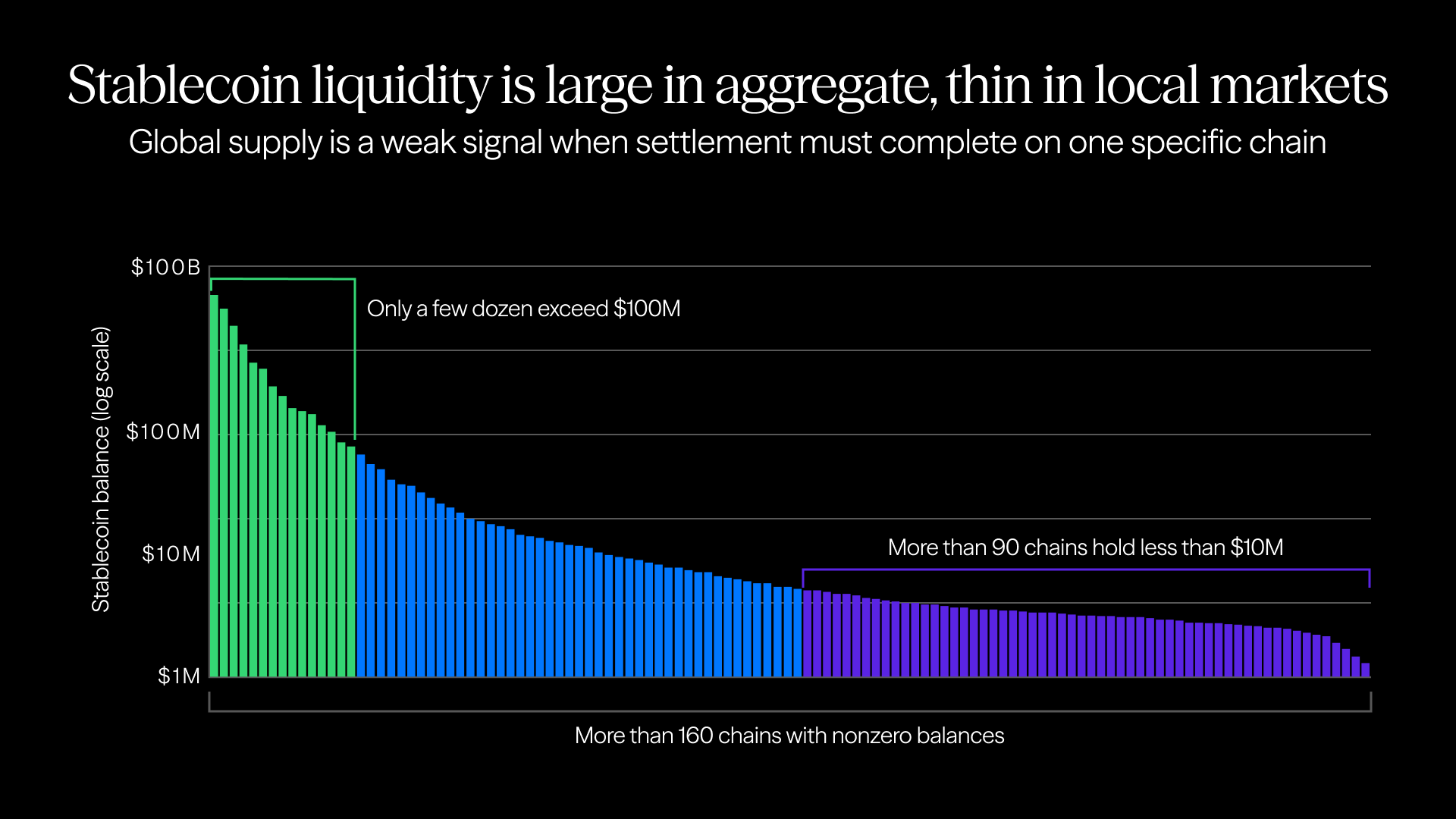

That problem shows up in the market’s shape. Across the stablecoin market, more than 90 chains hold less than $10 million in stablecoin value, while only a few dozen are above $100 million. The long tail matters because execution is local. A trade clears against the inventory and settlement conditions of the chain it lands on, not against global stablecoin supply. Read more on the distribution effect here.

Every new chain, issuer rail, and token format creates another execution context with its own local inventory and its own settlement conditions. So far, fragmentation has been most visible across one dimension, with the same instruments spread across more chains and venues. That market is now changing as new instruments arrive alongside institutional adoption.

The next phase of onchain finance depends on execution across fragmented forms of money. Crosschain connectivity helps, but price formation, fill quality, and settlement coordination still need their own layer. That layer has to take different forms of money across different money dimensions and orchestrate execution across them.

Think about a treasury or payments team. For them, global supply is a weak signal. What matters is whether the base asset can be converted into the right contra asset, on the right chain, with enough local settlement capacity to complete the transaction and avoid massive slippage. We built Superset for that layer of the market. Superset is the Unified Execution Layer for onchain FX.

The money dimension changes the market

The right starting point is the money hierarchy.

TradFi already distinguishes between forms of money. Monetary base, bank deposits, and money-market instruments all sit at different points on the liquidity and risk spectrum. Tokenization brings those distinctions onchain in a tradable form.

Superset’s framing uses four onchain categories:

- Digital M0: CBDCs and other direct central-bank liabilities in token form

- Digital M1: tokenized deposits or deposit tokens issued by banks

- Shadow M1: fiat-backed stablecoins issued by non-banks

- Digital M2: yield-bearing cash products such as tokenized money market funds or T-bill wrappers

Once money appears in multiple claim formats, a “dollar” stops being a single instrument. A deposit token is a bank liability. USDC is a claim on a non-bank issuer backed by reserves. A yield-bearing dollar token is a fund or product exposure with different liquidity and risk properties. They may all reference the same unit of account, but they do not behave the same way in execution or settlement.

Onchain FX is therefore broader than non-USD stablecoin trading. It includes same-currency conversion across money types. A treasury that holds tokenized deposits for safety may still need stablecoins for onchain operations. A payments firm that receives stablecoins may need bank-linked money for institutional settlement. A yield-bearing token may need to be converted into a payment-ready token before transfer. As more instruments and institutions come onchain, the examples increase.

This market can be described in two equivalent ways.

The conceptual view is:

- Currency

- Money tier

- Chain

The execution view:

- Chain

- Base assets

- Contra assets

These are the same market from different angles. Base asset and contra asset carry the currency and money-tier information. The chain determines where inventory sits, where the request enters, and where settlement must be completed.

That structure is what makes the market harder than familiar FX. Traditional FX mostly solves conversion across currencies within one dominant money tier. Onchain FX has to resolve three questions at once:

- Which asset is being sold?

- Which asset is being bought?

- On which chain does the trade have to settle?

A specific example makes this clear.

If the base asset is USDC and the contra asset is EURC, the trade is already an FX trade across currencies. If the request originates on Ethereum and needs payout on Base or Solana, chain fragmentation now shapes execution. If the base asset becomes a deposit token and the contra asset remains USDC, the trade is now same-currency but cross-tier. If the base asset is a yield-bearing dollar token and the contra asset is a payment-ready stablecoin, the conversion is again same-currency but cross-tier, with different settlement expectations.

The market fragments on a matrix, not on one axis. Routing alone cannot solve that problem. A router can search visible pools. It cannot create one coherent execution surface across many chains and many money forms.

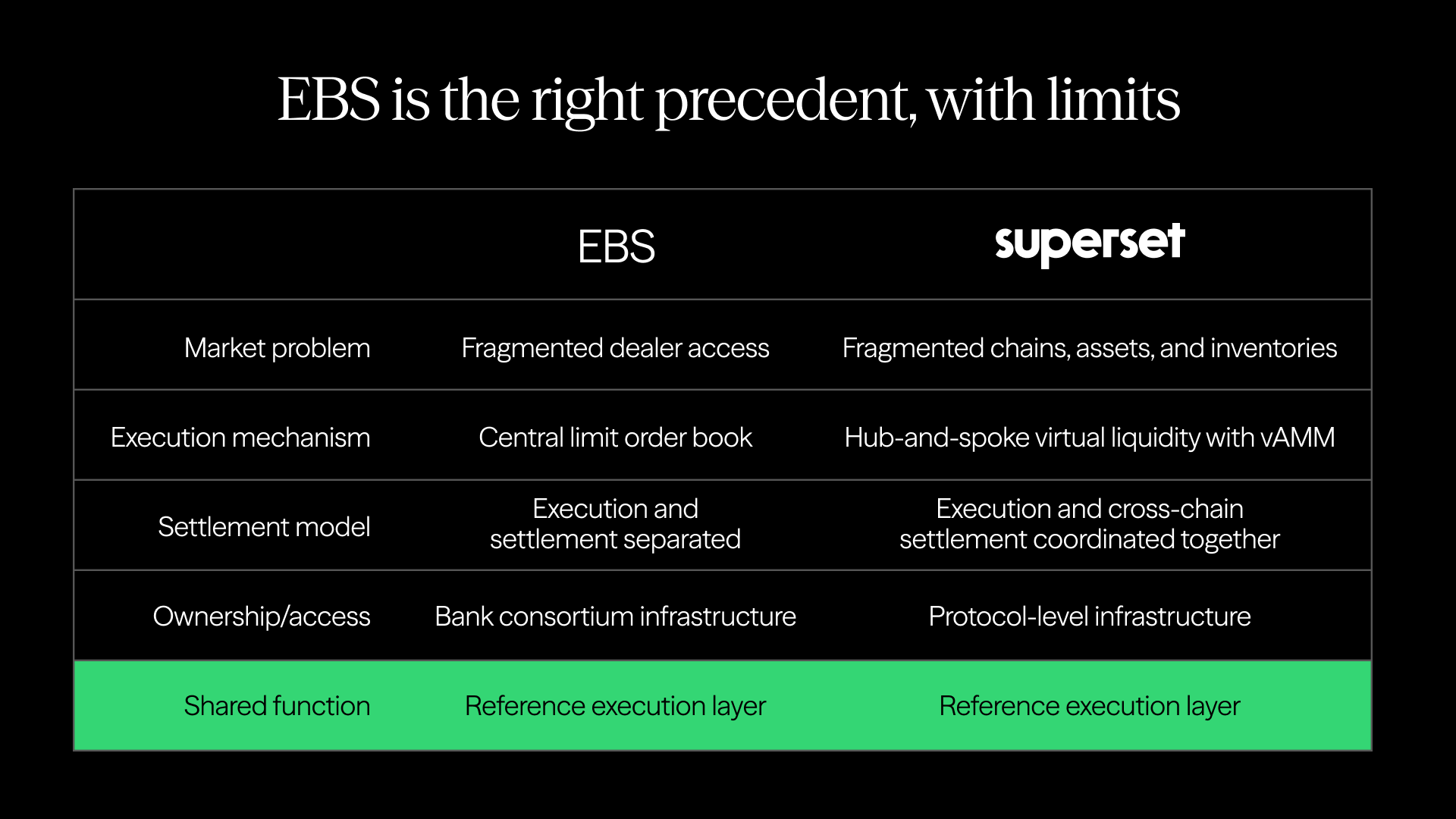

EBS is the right precedent, with limits

The EBS analogy is useful because it explains why execution layers matter. Before electronic broking became standard, interbank FX liquidity was scattered across bilateral relationships and broker networks. Dealers could not see the full market from one place. Execution depended on fragmented access. Size was harder to place. Price discovery was uneven.

By 2007, the Federal Reserve described EBS as the main venue for interdealer trading in EUR/USD and USD/JPY and captured its market role in one line:

"The reference price at any moment ... is the current price on the EBS screen."

That role persisted well beyond the first shift to electronic trading. EBS remained a core reference point for price discovery in major currency pairs and became embedded in how the market formed benchmark prices. That precedent matters for Superset. The useful parallel sits at the level of infrastructure function.

The similarities are clear

- Fragmented access weakens execution quality

- Partial depth produces worse fills in size

- Markets scale once execution becomes easier to reference and easier to trust

The differences matter just as much.

First, the cause of fragmentation is different. EBS dealt with fragmented intermediaries. Superset deals with non-interoperable chains, isolated token inventories, and different money forms.

Second, the mechanism is different. EBS used a central limit order book for professional dealer markets. Superset uses a hub-and-spoke virtual liquidity model with a virtual AMM (vAMM).

Third, the settlement problem is different. EBS sat on top of a traditional financial system that separated execution from final settlement. Superset has to coordinate execution and cross-chain settlement conditions inside the same protocol stack.

Fourth, the ownership and access models differ. EBS emerged from a bank consortium. Superset is protocol-level, open, market neutral infrastructure with a different adoption path.

Those differences lead to EBS as the right precedent for why neutral execution infrastructure becomes essential once currency markets fragment. It should be treated as a precedent, not a template. The distinction matters for institutional readers. The lesson is that fragmented markets need a reference execution layer if they want to support larger size, tighter pricing, and cleaner integration.

In onchain FX, that layer cannot just improve price discovery. It also has to work across fragmented chains, respect local inventory limits, and coordinate settlement conditions as part of the trade itself.

How Superset fills the gap

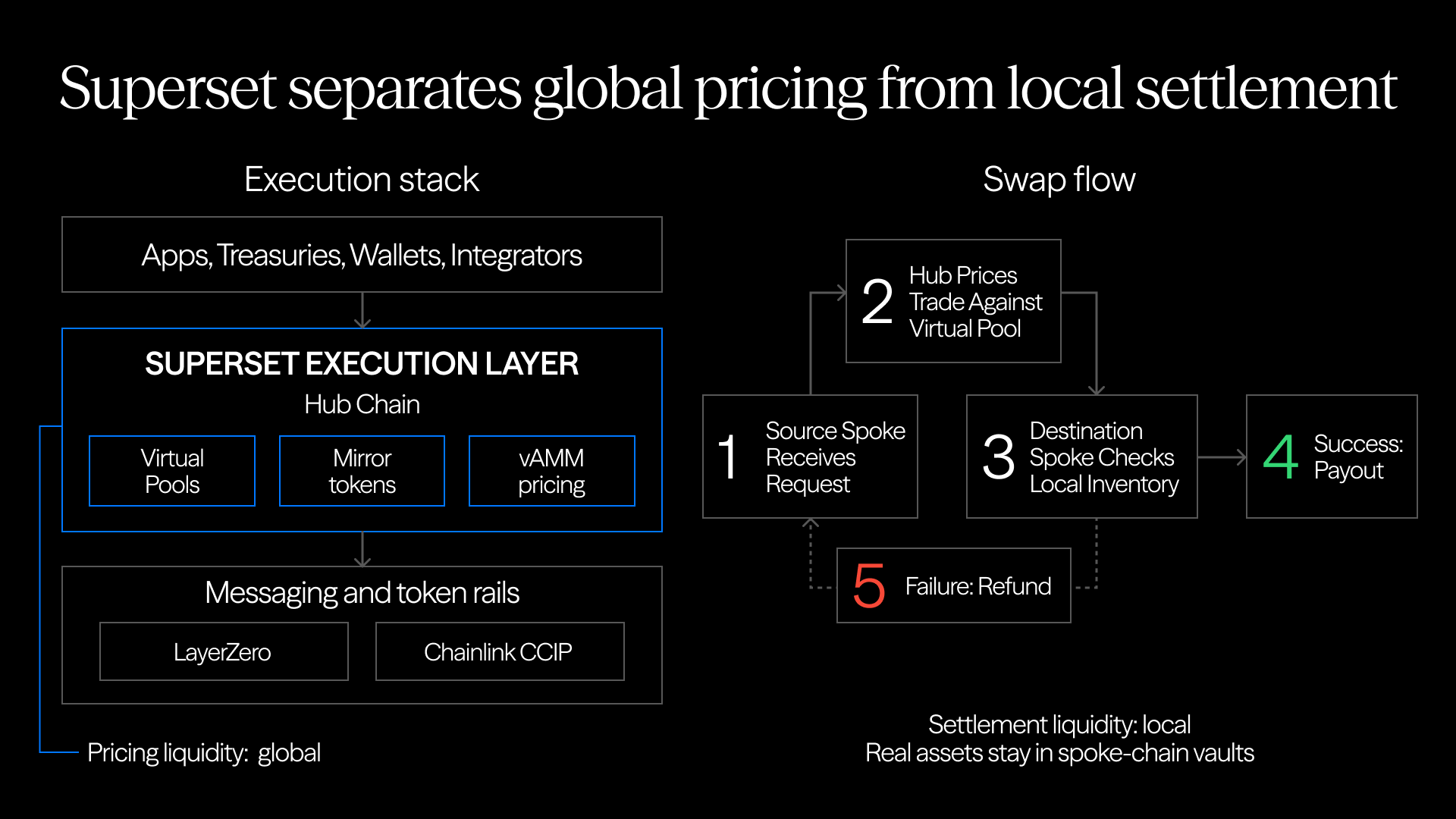

Superset is easier to understand by explaining its place in the stack. Messaging protocols coordinate data across chains. Bridges and token transport standards move assets. Superset sits above those rails. The crosschain request-response flow builds on robust messaging by LayerZero, while token support can also extend across standards such as Chainlink CCIP and Circle CCTP (USDC). The execution layer does a different job. It turns spread inventory into one pricing surface, decides how a trade is priced, and coordinates settlement once the price is set.

We focus on that layer. Superset uses hub-and-spoke virtual liquidity, virtual pools, and a request-response swap flow. Each virtual pool is a Uniswap V3 concentrated-liquidity pool deployed on the hub chain. Real assets sit in local spoke-chain vaults. The hub does not hold one giant crosschain pool. It maintains global state through mirror tokens and runs swap logic against those hub-side pools through a vAMM.

Trades are priced against hub-chain pool state, then settled with real assets from local spoke inventory. That creates a cleaner split between two functions that often get blurred together: pricing liquidity can be viewed globally, while settlement liquidity still has to exist locally on the payout chain.

A trade starts with five inputs:

- The source chain

- The base asset

- The contra asset

- The trade value

- The destination chain for settlement

The spoke forwards the request to the hub. The hub prices the trade against global virtual liquidity instead of one local pool. The destination spoke then pays out from local vault inventory if the documented conditions are met. If slippage, deadline, gas, or destination inventory checks fail, the documented path is failure plus refund. Execution is global. Settlement capacity remains local.

This changes the unit of execution. Without an execution layer, the trade sees local inventory first. Pricing quality and fill quality are shaped by the pool or route that happens to sit on that chain. In this model, the trade is evaluated in a broader decision context before payout is attempted on the destination side.

The architecture also makes the operational limits visible instead of hiding them. Rebalancing still matters. Local vault balances still matter. Messaging latency still matters. Realized execution still depends on where the inventory is available when the settlement has to be completed.

A market fragmented across chain, base asset, and contra asset needs three things: a wider decision context for pricing; explicit settlement coordination after pricing; a neutral utility that different issuers, apps, treasuries, and liquidity providers can all use. Superset’s architecture is designed around those needs.

The architecture also fits the institutional direction of travel. Circle’s EURC is available on Avalanche, Ethereum, Solana, and Stellar and that supported EURC can be swapped across supported blockchains through Circle Mint and its APIs.

Kinexys by J.P. Morgan positions its digital payments rail as an alternative to stablecoins for institutional cash settlements and reports average daily transaction volume above 2 billion across Kinexys.

Fnality frame is its payment system around real-time atomic settlement, 24/7 availability, and wholesale digital cash.Issuer proliferation is following the same path. Fidelity has launched FIDD, a dollar stablecoin for retail and institutional investors through Fidelity Digital Assets. The latest launch, Western Union and USDPT on Solana alongside a Digital Asset Network designed to connect stablecoins with real-world money movement.

The same expansion is showing up at the chain layer. Tempo is a blockchain for payments at scale and emphasizes stablecoin-native payments, tokenized deposits, and deterministic settlement. Arc is a Layer-1 built for stablecoin finance with direct ties to issuer and payments infrastructure. Canton is a public network for tokenized assets and institutional finance, with privacy and flexible application-level permissioning. More institution-focused chains mean more execution contexts, not fewer.

Those examples point in the same direction. The market is adding more forms of tokenized money, more issuer rails, and more chain environments, not converging on one. If those systems are going to coexist, an execution layer has to sit above them and orchestrate conversion across the full matrix.

Where value appears first

The strongest case for Superset appears in workflows that treasury desks, exchanges, and institutional issuers already have to run. Onchain money can look large in aggregate and still be thin where the trade needs to clear. Below are some real-world examples and applications that use live public pool depth to show the fragmentation problem the market already has to navigate.

Example 1: treasury conversion across currencies and chains

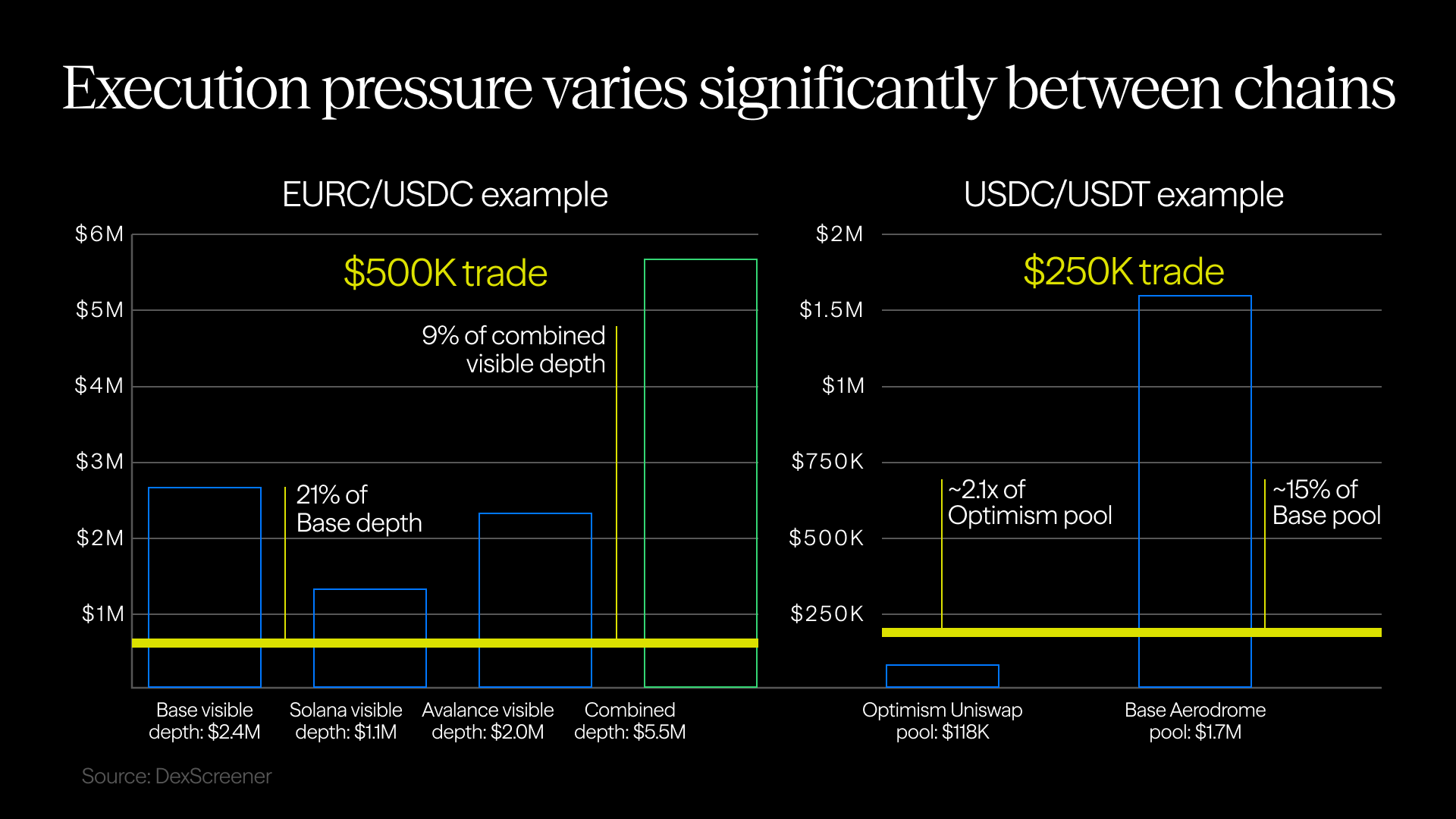

Take a treasury or fund operations team that receives USDC on Arbitrum from trading activity or OTC settlement and needs EURC on Base for EURO working capital, fund distributions, or settlement. The desk has to settle on Base. The execution question is whether price discovery is forced into Base-only liquidity or can reference the broader crosschain market first.

Visible EURC/USDC liquidity is split across separate local pools. This is the problem the virtual pool model is built to address. Instead of treating Base, Solana, and Avalanche as separate pricing environments, unified liquidity allows the trade to reference one broader execution surface before settlement is attempted on the destination chain.

Using public data (DexScreener), we can see ~$2.4 million of visible EURC/USDC liquidity across major Base pools, ~$1.1 million across visible Solana pools, and ~$2 million across visible Avalanche pools. A $500,000 conversion is therefore ~21% of visible Base depth, but ~9% of the visible depth across those three chain environments combined. That is the fragmentation pressure. Price impact depends heavily on which local pool is forced to absorb the order.

Source: DexScreener, Data as of March 10, 2026.

Local routing sees fragments. A unified execution layer is built to price against a broader market surface, then settle against local inventory where payout has to complete. The trade still depends on destination liquidity on Base. It is no longer framed as a Base-only pricing problem.

Example 2: rollup rebalancing inside the dollar complex

This example stays inside the dollar complex and shows why onchain FX is not limited to cross-currency trades. A payments firm or exchange treasury may hold USDC on Optimism and need USDC or USDT on Base for redemptions, collateral, or exchange settlement. The unit of account is still the dollar. The execution problem changes with chain, token representation, and local inventory.

Visible local depth can vary sharply even in this same-currency route. Using current data again, we see ~$118,000 of visible USDC/USDT liquidity on Optimism's main Uniswap pool. On Base, the main Aerodrome USDT/USDC pool is ~$1.7 million. A 250,000 rebalance is therefore a little more than 2x the visible Optimism pool, but only ~15% of the main Base pool. The same dollar conversion can be disruptive on one chain and routine on another. That is the operational version of the same problem.The same dollar conversion can be disruptive on one chain and routine on another. That is the operational version of the same problem.

Onchain FX is broader than foreign exchange in the narrow sense. Same-currency conversion can still behave like FX when chain and asset context change the execution surface. Superset matters because it treats that as one execution problem rather than a collection of disconnected local swaps.

Example 3: cross-tier conversion as institutional rails come onchain

The next example is same-currency, cross-tier conversion. A bank-linked digital cash instrument or deposit token may need to be converted into a public stablecoin for onchain activity, or public stablecoin balances may need to move back into a regulated settlement environment.

This application is slowly getting more traction every day. J.P. Morgan has piloted JPMD, a permissioned USD deposit token, on Base. That makes the institutional question easier to see. If a client can hold deposit-token dollars on Base but needs USDC or EURC for public-chain collateral, treasury movement, or settlement, convertibility becomes part of the product, not an optional add-on.

The public market is still early, so we do not yet see a clean, observable pool set like we do for stablecoin pairs. The execution need remains. Banks, issuers, and large treasuries will not want separate bilateral integrations for every chain, contra asset, and settlement rail. This is the gap between systems such as Kinexys, and public-chain liquidity. Once these instruments appear on more chains, convertibility becomes part of market structure besides product design.

Example 4: everyday payments and merchant settlement

The same execution problem shows up at the other end of the market. Stablecoins are not only treasury instruments. They are also being used for frequent, lower-ticket payments where cost, reliability, and failure handling matter as much as quoted price.

A recent Artemis analysis of Ethereum stablecoin transactions found that stablecoin payments and smart-contract transactions were roughly evenly split by transaction count. Inside the payment set, 67% of wallet-to-wallet transactions were labeled P2P, but they accounted for only 24% of payment volume. Stablecoin usage includes a high count of smaller-value money movement, not only institutional-size transfers.

BNB Chain provides a second signal from a lower-friction payment environment. Its half-year 2025 report says the gasless stablecoin campaign alone generated about $4.8 billion in gasless stablecoin volume and about 63,000 new wallets in the first 30 days. Lower-friction rails expand usage where transaction size is small and cost sensitivity is high.

For this audience, the constraint is different from a large treasury spot trade, but the infrastructure need is similar. A payments app, remittance flow, or merchant wallet may need to convert between local stablecoin balances and payout assets without making the user manage pools, bridges, or retry logic. On small transfers, failed routes, extra steps, or inconsistent execution can matter more than a few basis points of price.

This example makes the execution layer relevant beyond institutions. Superset can use the same unified liquidity and request-response model to support small-ticket conversion flows with explicit settlement and refund logic. Larger settlements and everyday payments are different operating environments. They still need predictable outcomes.

What this changes for integrators and capital

For applications and institutional integrators, fragmentation creates implementation overhead. A wallet, payments app, or embedded treasury product may want to support USDC into EURC, USDT into USDC, and future deposit-token into stablecoin conversion across Arbitrum, Optimism, Base, Solana, or other chain environments. Without an execution layer, each route becomes its own build. The application has to connect chain-specific pools, route logic, and failure handling. With Superset, the integration is framed once in terms of chain, base asset, contra asset, and settlement constraints. That opens the reachable liquidity surface while keeping the product and engineering model cleaner.

For market makers, LPs, and capital allocators, fragmentation shows up as inventory drag. In the EURC/USDC example alone, visible depth is split across Base, Solana, and Avalanche rather than presented as one market surface. In the dollar example, visible USDT/USDC depth differs sharply between Base and Optimism. That lowers utilization and turns inventory management into a larger operational job. The same capital base gets duplicated across more local pools while each pool serves a narrower slice of demand.

Superset does not remove inventory risk. It is built to solve fragmentation at the execution layer. LPs can support a broader demand surface through a unified execution model, while local balances and rebalancing determine where settlement capacity has to be restored. That is a cleaner setup for inventory management than duplicating capital route by route.

Why this can become the canonical reference

Stablecoins can keep expanding without a unified FX layer but institutional use cases will remain narrower and more operationally expensive if execution continues to rely on isolated local pools.

The market already has money onchain. It already has bridges, messaging protocols, issuers, and applications. What it still lacks at scale is a clean execution layer that can price and coordinate conversion across the full matrix of chain, base asset, and contra asset. That missing layer becomes more valuable as the money stack expands.

If the future includes public stablecoins, bank-issued deposit tokens, and wholesale digital cash systems operating in parallel, onchain FX stops looking like a narrow DeFi category. It starts to look like the conversion layer for tokenized money itself.

This is the gap Superset targets as neutral utility for a multichain, multi-currency, multi-tier market. The architecture supports that framing. The EBS precedent supports the market-structure logic behind it. Across issuers, settlement rails, and chains, the conclusion is that the money stack is already diversifying.

That role will be earned through liquidity density, rebalancing performance, integration adoption, and the ability to serve both public stablecoins and regulated money forms. As those conditions are met, Superset can become reference execution infrastructure for onchain FX.

References

BIS Triennial Survey: OTC foreign exchange turnover in April 2025 https://www.bis.org/statistics/rpfx25_fx.htm

Federal Reserve: Trading Activity and Exchange Rates in High-Frequency EBS Data https://www.federalreserve.gov/pubs/ifdp/2007/903/ifdp903.htm

BIS Quarterly Review: Downsized FX markets: causes and implications https://www.bis.org/publ/qtrpdf/r_qt1612e.htm

CME Group: Strengthening EBS Market: Building a Healthy FX Marketplace https://www.cmegroup.com/articles/2023/building-a-healthy-fx-marketplace.html

DefiLlama stablecoins dataset https://stablecoins.llama.fi/stablecoins

Circle EURC https://www.circle.com/eurc

Fidelity Investments expands digital asset investment lineup with stablecoin launch, Fidelity Digital Dollar (FIDD) https://newsroom.fidelity.com/pressreleases/fidelity-investments--expands-digital-asset-investment-lineup-with-stablecoin-launch--fidelity-digit/s/3b55e2d1-1dba-4120-9528-1e07e632f3f4

Western Union announces USDPT stablecoin on Solana and Digital Asset Network https://ir.westernunion.com/news/archived-press-releases/press-release-details/2025/Western-Union-Announces-USDPT-Stablecoin-on-Solana-and-Digital-Asset-Network/default.aspx?ref=blog.crossmint.com

Kinexys by J.P. Morgan https://www.jpmorgan.com/kinexys

Fnality https://fnality.com/

Canton Network https://www.canton.network/

Circle: Introducing Arc, an open Layer-1 blockchain purpose-built for stablecoin finance https://www.circle.com/blog/introducing-arc-an-open-layer-1-blockchain-purpose-built-for-stablecoin-finance

Tempo https://tempo.xyz/

J.P. Morgan: Kinexys by J.P. Morgan launches USD deposit token, JPMD, on Base https://www.jpmorgan.com/payments/newsroom/kinexys-usd-digital-deposit-tokens

Artemis: An empirical analysis of stablecoin payment usage on Ethereum https://www.artemisanalytics.com/resources/an-empirical-analysis-of-stablecoin-payment-usage-on-ethereum

BNB Chain half-year 2025 report https://public.bnbstatic.com/static/files/research/half-year-report-2025.pdf

DexScreener: Avalanche Uniswap EURC / USDC https://dexscreener.com/avalanche/0x975d4286bdB7b2989C8129f0B7C1299b166A11b3

DexScreener: Avalanche PHARAOH EURC / USDC https://dexscreener.com/avalanche/0x41FD792c9b83034c31666F602f4E315fbC2bD2eC

DexScreener: Avalanche Blackhole EURC / USDC https://dexscreener.com/avalanche/0x65f83CCacaBaAC4eD2f80289A02dF4D35d744aE8

DexScreener search: EURC / USDC pools https://dexscreener.com/search?q=EURC%20USDC

DexScreener: Base Aerodrome EURC / USDC https://dexscreener.com/base/0xc5E51044eB7318950B1aFb044FccFb25782C48c1

DexScreener: Solana Orca EURC / USDC https://dexscreener.com/solana/ArisQNcbjXPJD7RgPRvysatX3xcfHPTbcTkfD8kDoZ9i

DexScreener: Optimism Uniswap USDC / USDT https://dexscreener.com/optimism/0xa73c628eaf6e283e26a7b1f8001cf186aa4c0e8e

DexScreener: Base Aerodrome USDT / USDC https://dexscreener.com/base/0xa41Bc0AFfbA7Fd420d186b84899d7ab2aC57fcD1